TL;DR:

- Automated payment processing eliminates manual errors, delays, and fraud exposure in rental business payments. It increases efficiency, cuts costs, and improves fraud controls by replacing paper checks with electronic workflows. Implementing automation requires process redesign, supplier enrollment, and system integration for best results.

Automated payment processing is defined as a technology-driven system that handles business payments without manual intervention, consolidating approvals, payment execution, and reconciliation into a single workflow. For rental business owners and finance managers, the case is direct: manual payment handling creates errors, delays, and fraud exposure that automation eliminates. Platforms like Nomora and payment specialists like Corpay have demonstrated that automation cuts accounts payable (AP) time, reduces processing costs, and generates measurable financial returns. The Association for Financial Professionals (AFP) confirms that fraud risk from manual payments is at a record high. This guide explains why automating payment processing is the most effective operational decision a rental finance team can make.

Why automate payment processing: the efficiency case

Operational efficiency is the most immediate reason rental businesses switch to automated payment processing. Manual AP workflows require staff to log into multiple bank portals, re-enter data across systems, and chase approvals by email. Each of those steps adds time, and time in finance operations translates directly to cost.

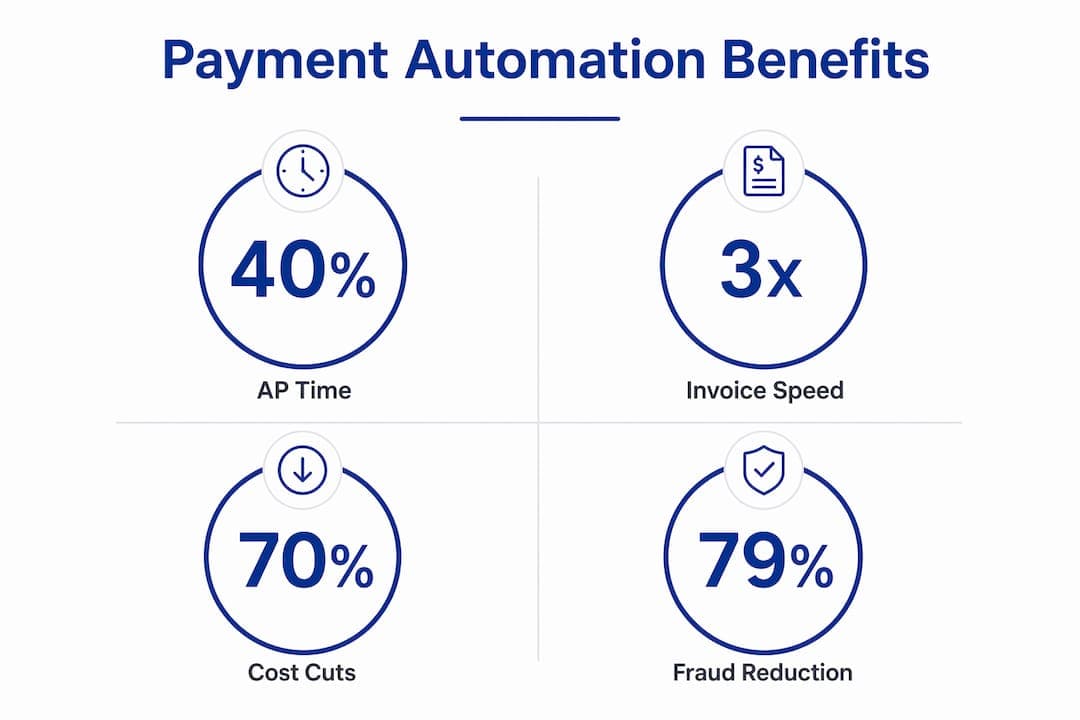

The efficiency gains from automation are well documented. AP time drops by 40%, invoices process up to three times faster, and manual processing costs fall by as much as 70%. For a rental business managing dozens of supplier payments each month, those numbers represent hours recovered every week.

Automation also closes a gap that invoice processing alone cannot fix. Invoice automation breaks down at the point of actual payment execution, where manual steps reintroduce errors and delays. Full payment automation removes those manual holds entirely, creating a continuous workflow from approval to settlement.

The operational gains compound when you consider reconciliation. Manual bank reconciliation consumes days each month and frequently surfaces errors too late to correct without cost. Automated systems match transactions in real time and flag discrepancies immediately, turning a multi-day monthly task into a continuous background process.

Here is how a consolidated automated payment workflow typically replaces fragmented manual steps:

- Invoice receipt and validation — the system captures invoice data automatically, removing manual entry.

- Approval routing — payment requests route to the right approver based on preset rules, with no email chains required.

- Payment execution — the system releases payment on the scheduled date via the correct method (ACH, virtual card, or wire).

- Remittance delivery — real-time remittance is sent to the supplier automatically, matched to the payment type.

- Reconciliation — transactions post to the ledger immediately, with alerts for any discrepancy.

Pro Tip: Integrate your payment automation platform directly with your ERP or accounting system via API. This eliminates duplicate data entry between systems and gives your finance team a single source of truth for all payment activity.

What cost savings does payment automation offer?

Cost reduction from payment automation comes from multiple directions, not just lower processing fees. Rental finance teams that treat automation purely as a cost-cutting tool often underestimate the full financial return.

The direct savings are significant. Automation cuts manual processing costs by up to 70% by removing labor-intensive steps from the AP cycle. Late payment fees disappear when the system releases payments precisely on their due dates rather than relying on a staff member to remember.

The less obvious financial advantage is rebate revenue. Corpay reports that its clients average $43,000 in annual rebates through virtual card programs. That figure represents money your rental business earns simply by routing supplier payments through the right payment method. At enterprise scale, the return is higher.

Key financial advantages of payment automation for rental businesses:

- Lower processing costs — eliminate manual labor from invoice handling and payment execution.

- Avoided late fees — precise payment timing removes the risk of missed due dates.

- Virtual card rebates — earn cash back on supplier payments routed through virtual cards.

- Working capital preservation — pay suppliers on the exact due date rather than early, keeping cash in your account longer.

- Reduced error costs — automated validation prevents duplicate payments and incorrect amounts.

Days Payable Outstanding (DPO) is a metric that measures how long a business takes to pay its suppliers. DPO management improves with automation because the system can release payments precisely on due dates rather than defaulting to early batch runs. Holding cash one extra day across hundreds of transactions adds up to a real working capital advantage.

| Financial benefit | How automation delivers it |

|---|

| Processing cost reduction | Removes manual labor from AP cycle, up to 70% savings |

| Late payment fee avoidance | Scheduled payments release on exact due dates |

| Virtual card rebates | Corpay clients average $43,000 annually |

| DPO optimization | Payments timed precisely to preserve working capital |

| Duplicate payment prevention | Automated validation flags duplicate invoices before payment |

How does automating payment processing improve fraud prevention?

Payment fraud is not a background risk for rental businesses. It is an active and growing threat. 79% of organizations faced payment fraud attacks or attempts in 2024, according to the AFP 2025 Payments Fraud and Control Survey Report. That figure covers businesses of all sizes, and rental operations with high transaction volumes are not exempt.

Checks are the most vulnerable payment method. Check fraud affects 63% of organizations that experience payment fraud. Automation directly reduces this exposure by replacing paper checks with electronic payment methods that carry built-in controls. Fewer checks in circulation means fewer opportunities for interception, alteration, or forgery.

The rental fraud prevention benefits of automation extend beyond simply removing checks. Automated systems apply validated banking data for every transaction, so payments go to verified accounts rather than manually entered details that could be wrong or fraudulent. Dual authorization controls require two approvers for payments above a set threshold, which blocks unauthorized transactions before they execute.

Fraud controls built into automated payment systems:

- Dual authorization — high-value payments require two approvers, blocking single-point fraud.

- Validated banking data — supplier account details are verified before any payment executes.

- Detailed audit trails — every transaction is logged with timestamps, approver names, and payment method.

- Automated remittance matching — payments are matched to invoices automatically, flagging unmatched transactions.

- Policy enforcement — payment rules apply consistently to every transaction, removing human override risk.

The primary risk of manual payments is the absence of centralized control and auditability. When payments run through spreadsheets and email approvals, there is no reliable record of who authorized what or when. Automation enforces those controls on every transaction without relying on individual discipline.

What should rental finance teams know before implementing payment automation?

Implementation success depends on treating payment automation as a process redesign, not a software purchase. Viewing automation as software only is the most common reason implementations underdeliver. The technology works, but it works best when the underlying payment process is redesigned around it.

The first practical step is supplier enrollment. Virtual card programs only generate rebates when suppliers accept card payments. Actively enrolling suppliers and validating their banking data before go-live determines how much of the financial benefit your rental business actually captures. Passive enrollment produces passive results.

Integration with existing systems is the second critical factor. Your payment automation platform needs to connect cleanly with your ERP, accounting software, or rental management system. Without that connection, staff end up maintaining two systems in parallel, which defeats the purpose of automation entirely.

Common implementation pitfalls and how to avoid them:

- Treating it as a plug-and-play tool — map your current payment process first, then configure automation around it.

- Skipping supplier enrollment — assign a team member to actively contact and enroll suppliers before launch.

- Ignoring integration requirements — confirm API compatibility with your accounting or rental management platform before selecting a vendor.

- Underestimating change management — train finance staff on the new workflow before go-live to prevent workarounds.

- Delaying reconciliation setup — configure real-time reconciliation from day one to capture the full time-saving benefit.

Pro Tip: Set up real-time reconciliation alerts from the first day of go-live. Catching discrepancies immediately prevents them from compounding into larger errors that take days to unwind at month-end.

Rental businesses that track rental payments with automated systems report the biggest gains in month-end close speed. When transactions post in real time, the close process shrinks from days to hours. That time goes back to analysis and planning rather than data cleanup.

Key Takeaways

Automating payment processing reduces AP time by up to 40%, cuts manual processing costs by up to 70%, and gives rental finance teams the fraud controls and financial visibility that manual workflows cannot provide.

| Point | Details |

|---|

| Efficiency gains are measurable | Automation cuts AP time by 40% and processes invoices up to 3x faster. |

| Cost savings go beyond fees | Virtual card rebates, avoided late fees, and DPO optimization add up to significant annual returns. |

| Fraud risk is real and current | 79% of organizations faced payment fraud in 2024; automation reduces check fraud exposure directly. |

| Implementation requires process redesign | Treat automation as an infrastructure change, not a software install, for best results. |

| Supplier enrollment drives ROI | Actively enrolling suppliers in virtual card programs determines how much rebate revenue you capture. |

The case for automation is stronger than most rental operators realize

Most rental business owners I speak with frame payment automation as a back-office convenience. They expect it to save a few hours a week and reduce some paperwork. The actual impact runs deeper than that.

The real value of payment automation is that it converts your payment process from an undocumented set of individual habits into a repeatable, auditable system. Payment automation as operating infrastructure is the right mental model. When your rental business grows from 20 vehicles to 200, your payment process needs to scale with it. Manual workflows do not scale. They just get more chaotic.

The fraud angle is the one that surprises rental operators most. They assume fraud is a problem for large corporations. The AFP data says otherwise. A rental business processing payments through paper checks and email approvals is a soft target. Automation closes that exposure without requiring a dedicated compliance team.

My honest advice: do not wait until your current process breaks down to make the change. The cost of a payment error, a fraud incident, or a missed rebate opportunity is always higher than the cost of implementing automation before those events happen. The automated bookings and payments model that leading rental operators use treats payment automation as a foundation, not a feature. Build on that foundation early.

— Dizzy

Rental businesses that want to put these principles into practice have a direct path forward with Nomora. Nomora's automated car rental payment software handles payment approvals, execution, and reconciliation within a single platform built specifically for the rental industry.

Nomora connects payment processing with reservations, fleet management, and contract data, so your finance team works from one system rather than switching between tools. The platform supports multiple payment gateways and integrates with accounting systems to keep your ledger current in real time. For rental businesses looking to reduce administrative overhead and strengthen financial controls, Nomora's rental software use cases page shows how the platform applies across different business types and sizes. Setup takes 24–48 hours, and the onboarding process is designed to get your team running without a lengthy implementation project.

FAQ

What is automated payment processing?

Automated payment processing is a system that handles business payments without manual steps, covering approvals, payment execution, and reconciliation in a single workflow. It replaces manual data entry, email approvals, and paper checks with rules-based electronic processes.

How much time can payment automation save a rental business?

Payment automation reduces AP time by up to 40% and processes invoices up to three times faster than manual methods. For rental finance teams managing high transaction volumes, that translates to hours recovered each week.

Does payment automation reduce fraud risk?

Yes. Automated systems replace paper checks with electronic payments, apply validated banking data, and enforce dual authorization controls. The AFP reports that 63% of payment fraud targets checks specifically, which automation largely eliminates from the payment mix.

What financial returns can rental businesses expect from payment automation?

Direct returns include lower processing costs, avoided late fees, and improved working capital through precise DPO management. Corpay clients also average $43,000 annually in virtual card rebates, a revenue stream that manual payment processes cannot access.

How long does it take to implement payment automation?

Implementation timelines vary by platform and integration complexity. Nomora's onboarding process is designed to complete in 24–48 hours for most rental businesses, with API integrations to accounting and ERP systems configurable during setup.

Recommended

Ready to streamline your car rental business?

Experience all the features mentioned in this guide with Nomora. Start your free 14-day trial today.