TL;DR:

- Rental businesses must track operating expenses like maintenance, insurance, taxes, utilities, mileage, and depreciation to ensure financial accuracy. Separating trust and operating accounts, reconciling bank statements regularly, and monitoring KPIs such as time and dollar utilization are essential for compliance and profitability. Automated systems streamline expense recording, improve accuracy, and support better decision-making.

Rental business expense tracking is the practice of systematically recording and categorizing every cost tied to rental operations so owners can protect profits and stay compliant. Without a structured system, deductible expenses slip through, cash flow becomes unpredictable, and tax season turns into a scramble. The IRS recognizes specific deductible categories under Schedule E, and industry KPIs like time utilization and dollar utilization only become meaningful when your expense data is clean and current. This guide gives rental business owners and financial managers a practical framework for building that system from the ground up.

What expenses does a rental business need to track?

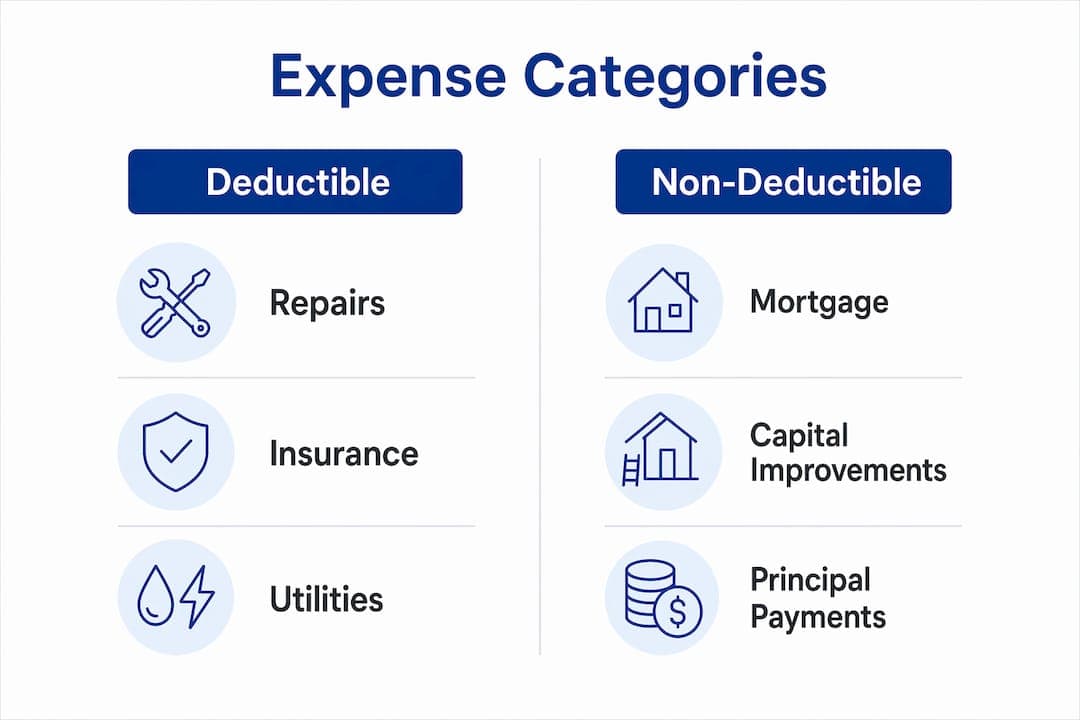

Rental expense management covers every cost that affects your net operating income. The IRS groups these into deductible operating expenses and non-deductible capital items, and knowing the difference directly affects your tax liability.

Deductible operating expenses include:

- Maintenance and repairs on vehicles, equipment, or property

- Insurance premiums covering liability, property damage, and fleet coverage

- Property taxes and licensing fees for each asset in your portfolio

- Utilities for any physical location tied to the rental operation

- Mileage for business travel related to managing rentals. The IRS mileage rate sits at 70 cents per mile as of june 2026. That rate applies to every qualifying trip you make to inspect, repair, or manage a rental asset.

- Depreciation on rental property over 27.5 years, or on equipment per the applicable MACRS schedule

Non-deductible items include mortgage principal payments and capital improvements. A new roof or a vehicle engine replacement adds to the asset's value and must be capitalized, not expensed in the current year.

Pro Tip: Keep a separate mileage log app or a dedicated GPS tracker for every vehicle used in your management activities. Mileage is one of the most commonly missed deductions in rental operations.

Rental businesses that manage vehicles benefit from integrating fleet GPS monitoring directly into their expense records. That data captures fuel costs, maintenance triggers, and mileage automatically, removing the need for manual logs.

How to set up a system for rental business expense tracking

The foundation of any reliable expense system is a standardized chart of accounts. Standardizing your chart of accounts across all rental properties or assets makes automated reconciliation and consolidated reporting possible. Without that consistency, comparing performance across units or locations becomes guesswork.

Spreadsheets vs. dedicated rental accounting software

Spreadsheets work for a single rental unit with low transaction volume. They break down fast once you add more assets, more tenants, or more payment types. Dedicated rental accounting platforms connect directly to bank feeds, scan invoices automatically, and match transactions to leases or contracts using reference numbers. That automation eliminates the manual entry that causes errors.

The table below compares the two approaches across key operational factors:

| Factor | Spreadsheet-based tracking | Dedicated rental software |

|---|---|---|

| Data entry | Manual, error-prone | Automated via bank feeds |

| Reconciliation | Manual matching | Reference-based auto-matching |

| Scalability | Breaks down past 5–10 units | Handles large portfolios |

| Audit readiness | Low | High |

| Reporting speed | Slow | Real-time |

Separating trust and operating accounts

Every rental business that holds tenant deposits or advance payments must keep those funds in a dedicated trust account. Mixing trust funds with operating funds is a common cause of audit failures and non-compliance. Open two separate bank accounts from day one and never transfer between them without a documented reason.

Pro Tip: Enter expenses weekly, not monthly. Weekly expense entry for a small portfolio takes only 10–15 minutes and prevents the data gaps that cause missed deductions at year-end.

How does bank reconciliation work for rental businesses?

Bank reconciliation is the process of matching every transaction in your accounting records to the corresponding entry on your bank statement. For rental businesses, this is not optional. Monthly reconciliation is a legal requirement for trust accounts, and high-volume operations with 50 or more units need weekly or even daily reconciliation to stay compliant.

The process follows a clear sequence:

- Pull your bank statement for the period and open your accounting ledger side by side.

- Match each deposit to a recorded rental payment, using the lease or invoice number as the reference.

- Match each withdrawal to a recorded expense, vendor payment, or owner distribution.

- Identify outstanding items. These are transactions that appear in one record but not the other. Flag them and investigate before closing the period.

- Clear all matched items and confirm that your adjusted bank balance equals your adjusted book balance.

- Document the reconciliation with a signed report and file it with your period-end records.

Leaving unresolved open items when closing your books produces an inaccurate general ledger. A cleared balance approach, where every item is tracked until matched, is the professional standard for rental financial statements.

Reference-based reconciliation using lease or invoice numbers is the most reliable method for rental businesses. It ties each payment directly to a specific tenant or contract, which eliminates allocation errors and makes audits straightforward. Manual reconciliation in Excel signals incomplete system implementation and delays your view of actual cash position. Automated reconciliation tools close that gap and accelerate your month-end cycle.

How does expense tracking connect to KPI monitoring and financial reporting?

Expense data is the raw material for every meaningful performance metric in a rental business. Without accurate cost records, your KPIs tell an incomplete story.

Two KPIs matter most for equipment and vehicle rental operations:

- Time utilization measures the percentage of time an asset is actively rented versus sitting idle. Time utilization below 65% signals a profitability problem that requires either better marketing or fleet reduction.

- Dollar utilization compares actual rental revenue to the replacement cost of the asset. A dollar utilization rate under 35% means the asset is not generating enough revenue to justify its cost.

Both metrics require accurate expense data to calculate net yield per asset. Tracking these KPIs weekly gives you the visibility to make pricing and fleet decisions before problems compound. Rental businesses that monitor fleet utilization weekly consistently outperform those that review performance only at month-end.

Reports every rental manager should generate monthly

Your expense tracking system should produce three core reports each month:

- Profit and loss statement (P&L): Shows total revenue minus total expenses for the period. This is your primary profitability check.

- Budget vs. actual report: Compares planned spending to real spending by category. Variances above 10% in any category warrant investigation.

- Owner statement: Summarizes income collected, expenses paid, and net distributions for each property or asset owner.

Break-even analysis ties directly to these reports. You calculate your break-even point by dividing total fixed costs by your gross margin per rental day. That number tells you exactly how many rental days you need each month to cover costs before generating profit. Expense tracking makes that calculation possible. For a deeper look at controlling costs at the unit level, the cost-saving strategies used by experienced rental operators provide a practical starting point.

What are the most common expense tracking mistakes rental businesses make?

Most expense tracking failures come from process gaps, not software limitations. The mistakes below are predictable and preventable.

- Skipping mileage logs. Mileage is fully deductible but requires contemporaneous records. A log created from memory three months later will not survive an IRS audit.

- Delaying data entry until tax season. Manual month-end entry misses 15–20% of deductible expenses compared to weekly recording. That gap translates directly into higher tax liability.

- Commingling trust and operating funds. Mixing these accounts creates compliance violations that can cost more to resolve than the original tax savings.

- Overrelying on spreadsheets. Spreadsheets do not flag duplicate entries, missing transactions, or reconciliation gaps. They require perfect human execution every time.

- Ignoring uncleared reconciliation items. Open items left unresolved when closing books corrupt your general ledger and make financial statements unreliable.

Pro Tip: Set a fixed weekly time block of 15 minutes to enter expenses and flag any bank transactions that do not match a recorded invoice. Consistency here prevents every problem on the list above.